School lunch debt sounds like a finance problem. It is, technically. But inside a school day, it becomes something messier: a student at the register, a parent who missed the balance notice, a staff member trying to follow policy, a food-service account that cannot absorb the loss forever, and a lunch line that still has to keep moving.

That is why the topic gets heated so quickly. Nobody wants a child caught in the middle of an account balance. Nobody wants school staff chasing families for money. Nobody wants a meal program quietly bleeding funds while food, labor, packaging, and delivery costs keep rising. Very noble mission. Very ugly spreadsheet.

This guide explains what school lunch debt is, why unpaid meal charges build up, what recent data says, and how schools can think about the operations around money, meals, communication, and handoff. It is not legal advice. It is a practical lunchroom guide for people trying to keep kids fed and the school day sane.

Key takeaways

- School lunch debt usually starts as unpaid meal charges on a student account, but it quickly becomes a budget, communication, and operations problem for schools.

- The School Nutrition Association reported that 92.2% of surveyed programs that do not offer meals free to all students had unpaid meal debt in Fall 2025.

- Debt is not only about whether families can pay. It can also grow from missed applications, unclear account notices, delayed payments, credits, absences, and messy point-of-sale workflows.

- Schools need a written meal charge policy, clear family communication, and a lunch workflow that keeps meals, money, and student handoff from colliding at the last minute.

- Buy My Lunch is not a public-meal-debt program. It helps schools running restaurant-prepared lunch keep parent orders, payments, labels, delivery details, and credits organized.

What school lunch debt actually means

School lunch debt is usually the unpaid balance created when a student receives a paid meal but the account tied to that student does not have enough money to cover it. Schools may call it unpaid meal charges, delinquent meal payments, negative balances, or bad debt once it reaches a certain accounting stage.

The label matters because different stages can trigger different handling. A low balance notice is not the same as a delinquent account. A temporary negative balance is not the same as debt that must be written off. Schools participating in federal meal programs are expected to have clear policies for unpaid meal charges, and USDA keeps guidance on unpaid meal charges as part of the school nutrition program conversation.

The human version is simpler: lunch was served, payment did not happen, and someone now has to decide what happens next. Does the child still receive the regular meal? How is the family notified? Who follows up? How long can the account stay negative? Which funds can and cannot be used to cover the balance? What happens at the end of the school year?

Why unpaid meal charges build up

It is tempting to treat lunch debt as a simple failure to pay. That is too thin. Families fall behind for many reasons: income changes, missed free or reduced-price meal applications, confusing account portals, delayed deposits, language barriers, lost notices, split households, or eligibility rules that do not match how tight the month feels.

The school process can add friction too. A family may not know an account is low until the balance is already negative. Staff may not have a clean way to distinguish a one-day issue from a recurring problem. Meal systems may not communicate clearly with families. Credits, absent students, refunds, second meals, a la carte items, and account carryovers can make the ledger harder to understand than it needs to be.

This is why a strong meal charge policy is only one piece. The daily workflow matters just as much. Schools need account visibility, predictable notices, a clear escalation path, and staff training so the policy does not turn into improvisation at the register. Lunch lines are terrible places to make sensitive family-finance decisions.

What recent school lunch debt data shows

The current public data makes the scale hard to wave away. The School Nutrition Association's SY 2025-26 Trends Report found that 51.9% of all surveyed school nutrition programs reported unpaid meal charges or debt in Fall 2025. Among programs that did not offer meals free to all students districtwide, the share rose to 92.2%. The same report showed $25,288,737 in total accumulated debt among 643 reporting districts. SNA's SY 2025-26 report also notes that reported debt ranged from $5 to $4,000,000.

SNA's public school meal statistics page summarizes the same pressure in plain terms: when families cannot or do not pay for meals served, unpaid meal debt can quickly accumulate and force schools to cover losses with education funds. That is the part that turns an account balance into a school budget issue.

The debt pattern also changes when meals are free for all students. In the SNA report, 23.3% of programs offering meals free to all students districtwide reported unpaid meal debt, compared with 92.2% of programs not offering all meals free. That does not mean every school can or should use the same funding model. It does show why universal meal options, state policy, Community Eligibility Provision, and local budget support are so central to the lunch debt conversation.

Where Community Eligibility fits

The Community Eligibility Provision, usually shortened to CEP, is one reason some schools can serve breakfast and lunch at no cost to all enrolled students. USDA explains that CEP allows eligible high-poverty schools and districts to serve meals to all students without collecting household applications. For qualifying schools, that can remove a lot of account-balance friction because families are not paying student by student at the point of service.

CEP is not a magic wand. It depends on eligibility, claiming rules, reimbursement calculations, and whether the school can cover any costs above federal assistance. Some states also fund free school meals more broadly. SNA's 2026 position paper notes that, at the time of its report, nine states had dedicated permanent state funds to provide free school meals. SNA's 2026 position paper frames free-meal access and reimbursement as major policy priorities.

For a school operator, the practical point is this: know which model you are actually running. A federally reimbursed meal program, a state-supported free-meal model, a parent-paid private-school lunch program, a caterer, and a restaurant-prepared ordering system all handle money differently. Confusing those models leads to bad decisions and worse parent communication.

The operational problem behind the debt

School lunch debt grows in the space between policy and daily reality. A policy may say when families are notified. The actual workflow decides whether the notice is clear, timely, translated when needed, and easy to act on. A policy may say a school will collect unpaid balances. The daily process decides who makes the call, what tone they use, and whether the family understands the options.

The same goes for the meal itself. If the student account is negative, the school needs a plan that protects student dignity, follows applicable rules, and keeps the lunch line from turning into a public accounting desk. Staff should not be left guessing. Parents should not be surprised. Students should not become messengers for a billing process they do not control.

Good operations do not eliminate every unpaid balance. They reduce confusion. They make the next step obvious. They keep sensitive conversations away from the serving line. They also help schools spot the difference between a family that needs application support, a payment-system problem, a recurring account issue, and a one-off missed deposit.

A practical school lunch debt checklist

Schools reviewing unpaid meal charges should look beyond the balance total. The better question is where the process is breaking.

- Is the meal charge policy written clearly enough for families and staff to understand?

- Are low-balance notices sent early, often, and through channels families actually use?

- Can families see balances, payments, credits, and charges without calling the school office?

- Is free or reduced-price meal application support easy to find before debt grows?

- Do staff know what to do at the point of service when an account is negative?

- Are second meals, snacks, a la carte items, absences, and refunds handled separately from reimbursable meals?

- Who reviews accounts before year-end, and what funds are allowed to cover unresolved balances?

- Does the school track patterns by grade, campus, payment method, communication channel, or time of year?

- Are families treated with dignity even when the school has to follow collection rules?

That list is not glamorous. It is the work. Lunch debt becomes much harder when nobody owns the details until the balance is already a problem.

What private schools should learn from the debt issue

Private schools may not be operating inside the same public-program structure, but the lesson still applies. If families pay for lunch directly, the school needs clean rules around ordering, payments, credits, missed deadlines, refunds, absent students, menu changes, and who handles parent questions.

A private-school lunch program can avoid the phrase "school lunch debt" and still create the same operational drain. A parent thinks they ordered. A student is absent. A restaurant prepared against the wrong count. A credit does not show up. A menu cutoff was missed. The office gets pulled in because lunch is emotional, visible, and happening right now.

That is why schools should compare lunch models by total friction, not only meal price. The useful comparison is the full cost of school lunch: family payment, school subsidy, staff workload, vendor coordination, communication burden, delivery accuracy, and the handoff moment students actually experience.

How Buy My Lunch fits the conversation

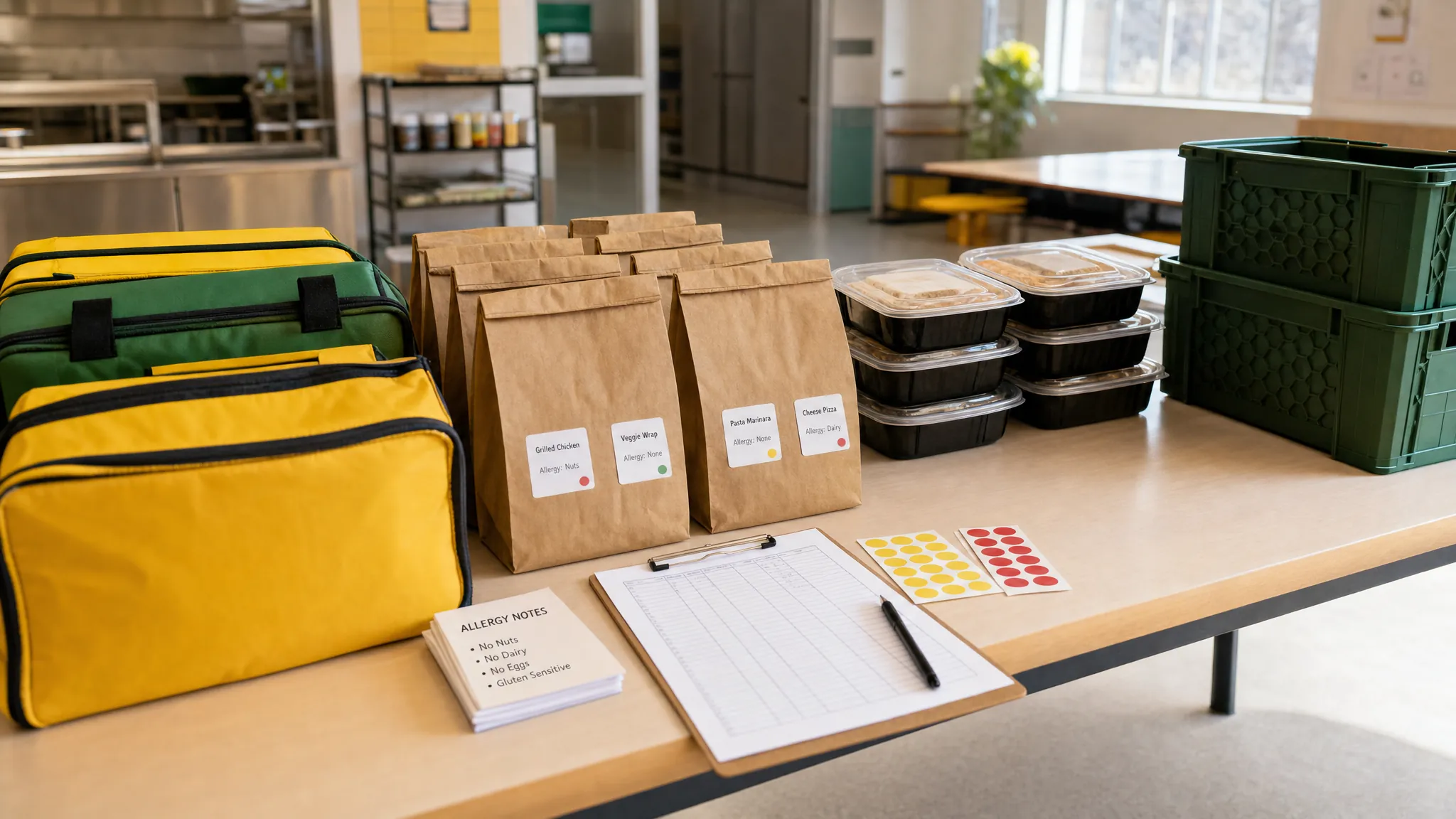

Buy My Lunch does not replace federal meal programs, decide school meal policy, or erase public-school meal debt. Different problem, different lane. What it does solve is the restaurant-prepared lunch workflow for schools that want families to order ahead from local restaurants without turning school staff into order takers, payment chasers, label makers, and delivery detectives.

Families order through the app at participating schools. Restaurants prepare against organized counts. Meals arrive labeled for the student handoff. Payments, credits, order cutoffs, school-specific menus, delivery details, and restaurant prep all live in one connected flow instead of scattered emails, envelopes, spreadsheets, and hallway favors.

For schools comparing options, that operating layer matters. A lunch model is only as strong as its weakest daily detail. If the food is good but payments are confusing, lunch still becomes a front-office problem. If parents have choices but restaurants get messy counts, lunch still gets weird. If meals arrive but labels are unclear, somebody still has to play detective with a stack of bags.

The broader takeaway from school lunch debt is not that every school needs the same model. It is that money, meals, communication, and handoff cannot be treated as separate systems. They meet in the lunchroom. Schools that understand that build better lunch programs, whether they are running a federal meal program, a private-school catering model, or a parent-paid restaurant lunch option.

For more context, the Buy My Lunch school lunch statistics page tracks current numbers on participation, cost, meal debt, food waste, and school lunch operations. Schools comparing lunch models can also review online lunch ordering for schools and the lunch programs for schools guide.

Frequently asked questions

What is school lunch debt?

School lunch debt is the unpaid balance that can build up when a student receives paid school meals but the family account does not have enough money to cover them. Schools often call these unpaid meal charges. Once they accumulate, the issue can affect family communication, school budgets, and the daily lunch workflow.

Can schools use federal meal funds to pay off lunch debt?

Schools generally need to treat unpaid meal balances carefully because federal child nutrition funds are meant for allowable program costs, not for writing off bad debt. Specific rules and accounting treatment can vary by program and state guidance, so schools should confirm requirements with their state agency or qualified adviser.

Why does lunch debt keep happening if free and reduced-price meals exist?

Eligibility programs help many families, but they do not remove every gap. Some families miss applications, do not qualify even though money is tight, lose eligibility, have delayed paperwork, or fall behind on account payments. Debt can also grow when notices are unclear or account systems are hard for families to track.

What can schools do to reduce unpaid meal charges?

Schools can keep the meal charge policy clear, communicate low balances early, make account information easy to find, help eligible families complete applications, review whether universal meal options are available, and tighten the daily process around orders, payments, credits, and absences.

Is school lunch debt the same issue for private schools?

Private schools often have a different lunch model, but the same friction can appear in another form: unpaid balances, parent questions, credits, missed orders, unclear cutoff rules, and staff time spent sorting lunch problems. The exact policy context is different, but the operational lesson is similar.

How does Buy My Lunch help with lunch payment friction?

Buy My Lunch helps schools offer restaurant-prepared lunch through organized family ordering. Parents order ahead, restaurants prepare against real counts, meals arrive labeled, and payments, credits, cutoffs, delivery details, and handoff steps stay connected.

Related posts

School Lunch OperationsHow Does the National School Lunch Program Work?

School Lunch OperationsHow Does the National School Lunch Program Work?A practical guide to how the National School Lunch Program works, who pays, what schools manage, and where private lunch options fit.

School Lunch OperationsPrivate School Lunch Cost for K-12A private K-12 guide to what school lunch really costs: cafeterias, restaurant partners, tuition-included models, parent-paid meals, and handoff.

School Lunch OperationsFood Waste in Schools: A Practical Lunchroom Guide

School Lunch OperationsFood Waste in Schools: A Practical Lunchroom GuideHow schools can think about food waste, ordering, share tables, composting, packaging, and restaurant-prepared lunch without creating more lunchroom chaos.